Talk:Credit card/Archive 1

| This is an archive of past discussions about Credit card. Do not edit the contents of this page. If you wish to start a new discussion or revive an old one, please do so on the current talk page. |

| Archive 1 |

Jane Bryant Quinn on sub-prime cards (April 2007)

She has an article in the April 9, 2007, issue of Newsweek, p. 49: “When the card arrives, however, your line might be only $250. And then come the fees! "Program" fees. Account set-up fees. Participation fees. Annual fees. They're charged to your tiny credit line, leaving you almost nothing to spend.” “Take the First Premier Bank Gold Card, at 9.9 percent interest with a $250 line. After charging upfront fees, however, you start out with a debt of $178 and just $72 extra to spend.” [1]

I am often on the other side of wiki controversies, because I want it to be real, and a lot of people seem to want it to be safe, or “neutral.” I want it to be cutting edge enough that the business student in college or the consumer looking something up, will actually learn something real. And maybe even enough cutting edge stuff toward the end of the article, that the seasoned businessman or businesswoman at age 50 thinking about doing something in the credit card business might actually learn something, too.

Now, our article here is better than the average wiki article. We include the class action suit about “rolling back” posting times and the documentary film “Maxed Out.” And if someone wants to include the other side about customer irresponsibility, fine, we can include summaries and references about that side, too. In fact, we need not limit it to only two sides. Most complex issues have multiple facets, many, many of which are worth discussing. And along with this comes the value of allowing the article to be long. We can have a reasonably lengthed introduction, and then we can let the article itself become longer and longer, and better and better, and richer and richer. Afterall, bandwidth is relatively cheap FriendlyRiverOtter 22:52, 23 April 2007 (UTC)

What the fuck are you babbling about. People come here to learn, not wade through bullshit. - 97.88.194.246

Very useful survey on credit cards

Can be found at http://www.banking.state.ny.us/intrate.htm It tells which cards have the controversial Universal Default Clause, double cycle billing etc.

canada ??????????

what is so special about canada to have its own section in the article !!!

--I concur. Besides, it's semi-incorrect. The "interactive tool" does not exist in FCAC site. The closest is a credit card calculator which is provided by Industry Canada.

The words "due date" in the sentence below are for some reason hyperlinked to the movie Expiration, which is a Canadian film that has nothing to do with credit cards as far as I can tell. I don't know what this is supposed to be pointing at or even if it should be pointing at anything at all, so I'll throw it out there for someone who knows what they're doing.

"Otherwise, the cardholder must pay a defined minimum proportion of the bill by a due date, or may choose to pay a higher amount up to the entire amount owed."

Please append this section with a comment or delete my comment when it is fixed so it is only fixed once. Thanks! 68.115.107.36 07:01, 27 March 2007 (UTC)

single use credit cards?

I would like to find out more about this. If anyone here has good information to share, perhaps you could add it to the security section? That way my bank or credit card company would know my permanent credit card but the non-trusted or semi-trusted vendor would only have a single-use credit card number to add to their insecure database.

One-time single-use disposable

The consumer can prevent on-going fraud by using special one-time single-use disposable credit card numbers, generated for each individual transaction. These special numbers can include custom limits on the transaction amount and a short-term authorization/expiration date.[2] Even reputable main-stream online vendors are forcing customers to agree to automatic subscription renewal charges and making it very difficult to opt-out.[3] [4] Single-use numbers are a way for the consumer to take back control. 69.87.199.244 12:12, 8 January 2007 (UTC)

Also, perhaps the a.K.a Card should be added to the security section? 144.92.81.181 16:16, 13 June 2007 (UTC)

no dot coms?

I re-listed one page on external links. It's a dot com, but the one particular page of the site seemed useful, the list of credit cards. Are dot com sites automatically not allowed in wikipedia?

UPDATE: reverted this again, specifically the credit card list from indexcreditcards.com. Anyone have feedback on this, especially Texture, who has taken that link down?

- Please review Wikipedia:External links and WP:SPAM for guidance on appropriate links. - Tεxτurε 16:40, 15 December 2005 (UTC)

I have, and under External Links there's this:

Maybe OK to add

Web directories: When deemed appropriate by those contributing to an article on Wikipedia, a link to one web directory listing can be added, with preference to open directories (if two are comparable and only one is open). If deemed unnecessary, or if no good directory listing exists, one should not be included.

My thought is that the list of credit cards seems like a good directory. I know the overall site is commercial, but that particular page seems like a useful resource -- I can't imagine those are all advertisements in that list, some of them look pretty obscure.

Thoughts from others?

too much opinion?

Under "Security", currently states: "Contrary to what credit card companies advertise, many times the consumer is held liable for fraudulent charges and their high-paid lawyers ensure that the burden of proof lays with the consumer."

Like the point before, no proof that this statement is true, and phrase "high-paid lawyers" suggests the writer has a personal beef with the credit card industry that is being stated as fact.

Am deleting the above sentence, but leaving it here in case of dispute.

too much opinion?

Under "Features", currently states: "In theory, some countries such as the United States limit the amount that a consumer can be held liable for fraudulent transactions with the intention to shift the liability to the merchant. In reality, however, merchants and credit card companies are always trying to hold the consumer liable."

This seems to state as fact what can't be proven -- how are merchants and credit card companies always trying to hold the consumer liable? In most cases, credit card companies limit consumers' liability because they don't want them to get soured on using credit cards -- they'll take a hit on fraud due to stolen credit cards on the bet that they'll make up that money over the long haul by the consumer continuing to use their credit card.

Am changing that paragraph, but left the original in this message in case of disagreement.

math error?

- you must first put down a deposit between 100% and 150% of the total amount of credit you desire. Thus if the holder puts down $1000, he or she will be given credit in the range of $1000–$1500.

If $1000 is 150% of an amount, the original amount must be $666.67. So the question is do you need to put down more than you borrow or less then you borrow? Pretzelpaws 18:13, 18 August 2005 (UTC)

Is there any source of the information about the discover bank now using BINs 650000-650099? I cannot find any supporting data about this. Kazriko 00:34, 1 November 2005 (UTC)

"A credit card user are issued after approval from the provider ... " doesn't make sense. Nor does: "Secure credit cards are an advantage to anyone with, without, or with poor credit history." www.danon.co.uk

--- I agree: Propose to substitute "After a successful credit check, the consumer is issued a credit card by the Issuing financial institution." and #2 "Secure credit cards are intended for either persons with prior history poor credit, or people seeking to develop a good credit history."

Credit card numbering

The section that descibes how American Express cards are numbered doesn't seem right. If only 4 of the digits are used for 'account number', they would be extremely limited in the number of accounts they could have. What gives? ike9898 17:27, 30 November 2005 (UTC)

Cardholder Liability

What is the source of this claim: " Contrary to what credit card companies advertise, many times the consumer is held liable for fraudulent charges and their high-paid lawyers ensure that the burden of proof lays with the consumer." VISA Regulations require that the MAXIMUM a cardholder can be held liable for is $50 of any fraudulent activity. Mastercard has a similar policy. In practice, few issuers enforce the $50 maximum, and pass-on zero liability to the consumer. The only exception is when a customer disputes a charge that they were legitimately involved in and consented to. In these cases it is not a fraud or security concern.

What is the risk faced by the acquirer bank in case of default by the customer? does he get his cut even if the customer defaults or does he even bear the risk?

- This is one of the primary advantages to the merchant. The merchant does not have to worry about payment. The credit card issuer guarantees the payment (provided the merchant adheres to the rules; get authorization, signature, card present, etc...) The credit card issuer bears the risk of default by the customer.

This is true only when the merchant follows all guidelines for each respective card environment - SWIPED or CARD-NOT-present. Also true that all authorization, signatures must be present...but important to include using only matching billing address for auth & shipmentand even CV2 or CVV verifyiers are in place. Registration w/ 'Verfied by Visa' program works to shift the risk liability back to card issuers. Devinma 21:16, 23 May 2007 (UTC)

Choosing and using link

Please do not remove the choosing and using link thinking it is a commercial site. Please see note below from Stollery - a Moderator for VandalProof: I have readded the link but reworded the description - I would suggest you also post a note on the talk page stating what you told me, and referring people to www.APACS.org.uk for more info. Hope this helps - Glen TC (Stollery) 12:49, 23 May 2006 (UTC) Thanks.

- I reverted your last change. I do agree that the link is worthy of inclusion. However, it cannot be called impartial if the site is maintained by an industry body. --GraemeL (talk) 13:22, 23 May 2006 (UTC)

Credit card use lessens tax avoidance and thus entitled to positive discrimination

> The end result is that cash consumers are essentially subsidizing credit card holder purchases

This is all right, since the government has fair desire to make sure that all monetary transactions are conducted with legal (tax payed) fiscals. A huge percent of cash transactions are conducted with illegally obtained money (criminal gains) or money, who origin did not pay tax. This is impossible with credit cards, because the banks have computerized record of all money flow and therefore illegal income is easily discovered. Thus the government is fully within its own right to encourage credit card use among the citizens, even at the expense of cash users, because all countries of the world have it written in their constitutions that taxes must be paid. Cash use is the foremost vector of tax avoidance and thus best eliminated.

--Citation please.

Nonsense?

I was under the impression that banks lend as _much_ of their capital as they can. The reserve requirement is there to make them _keep_ some of it on hand to pay back their creditors, not to ensure that they loan a portion of it out. As far as I know, there is nothing stopping a bank from borrowing 100$ to lend 100$, but this article implies that they _must_ loan 6$ directly from their reserves. There is also nothing about this on the reserve requirement page. What this probably _should_ say is that "Banks generally borrow the money that they lend to their customers. As they receive very low-interest loans from other firms, they may borrow as much as their customers require, while loaning their capital to other borrowers at higher rates.

Does the old version actually make sense? "Banks generally lend as little of their own capital as the Federal Reserve requires. For example, if a bank's credit card portfolio consists of $100 Billion in loans to consumers, and the reserve requirement is set at 6%, the bank will lend $6 Billion of it's own funds, and go to capial markets to borrow the other $94 Billion. The interest rate large banks receive in such transactions is relatively low, usually only slightly above the fed funds rate, but even 6% on $94 Billion adds up quickly."

Therealhazel 05:39, 25 June 2006 (UTC)

- That edit was US centric but has been fixed now. Banks will want to lend as much as they can by borrowing at a lower rate from governments etc. There is no reason for banks to have any sizable reserve except for local regulations (which vary) to keep banks safe from bankruptcy. --Clawed 11:25, 25 June 2006 (UTC)

- I've only taken US centric econ, so that's all I knew :D. Thanks for cleaning it up. I don't know _what_ that other stuff was. --Therealhazel 16:42, 28 June 2006 (UTC)

Creditors can/do use debt instruments that allow them to comply with the Truth in Lending Act (TILA) in that no money is actually lent to the credit seeker, rather the credit seekers own money is used. Basically, the creditor goes into debt by accepting the credit seekers application to be in debt, which draws from the 3rd and 4th parties own pools of debt and all other financial gains by that creditor or its assignees (i.e, these debt instruments can be loaned, traded or sold for profit, which is quite lucrative). This is one way it is done. Ken 63.139.73.5 16:27, 10 August 2007 (UTC)

"Credit Card Expiration Dates Are Obsolete"

http://itmanagement.earthweb.com/columns/executive_tech/article.php/3607996

Stoozing?

Shouldn't there be a link to stoozing in here somewhere? (a5y 00:09, 5 August 2006 (UTC))

Credit Card Tax

- In some areas, such as Ireland, governments profit from credit cards through the imposition of a stamp duty or credit card tax. This is usually done where a cheque tax previously existed. This tax is taken automatically from the account, just like a purchase, by the bank on behalf of the government annually. This tax—unlike its cheque counterpart—is payable in arrears so no refund is possible.

I removed this from the profit/loss section because it didn't fit.. however I still think its good.. Going to look for somewhere to put it. Cliffb 16:24, 9 August 2006 (UTC)

- Seems good - bung it in! Also, is this on the consumer's head, or the CC companies? leopheard 13:17, 3 March 2007 (UTC)

No Citations?

The page is full of statements with no citations, specially the #Controversy section. It would be better if we could add some citations, otherwise this all looks like 'any one can change it, whats the point' arguemnt I generally have to listen when I refer to wikipedia :)--Anupamsr 20:11, 9 August 2006 (UTC)

Credit on Credit Cards

I have a doubt about how credit and interests on a credit card are calculated.

I understand APR is a yearly percentage and that when calculating interest banks or credit card companies use a Monthly Periodic Rate (MPR) which is 1/12 of the APR.

I also understand that in most cases there is a minimum monthly payment which is a small percentage that must be paid in order to remain in good standing.

My first question is, What is "Finance Charge"? I was told this is the interest charge on your outstanding credit card balance, is this the same than APR?

I've now got an example, I would appreciate if you could go through it and tell me if that is the way credit is worked out and if not what I calculated wrong, Thank you.

APR = 16.8% MPR must be: 1.4% Minimum Monthly Payment = 2% Finance Charge = ??

If the customer's outstanding balance is £350 and he pays £200.

Interest = 1.4% of £350 which is £4.90 £200 payment - £4.90 interest = £195.10 New Balance = £350 outstanding balance - £195.10 = £154.90

Is this correct?

What would the Minimum Monthly Payment be? Would it be £11.90? [2% of £350 (£7) + MPR (£4.90)]

Thank You.

![]() Paddy :-) 03:34, 11 August 2006 (UTC)

Paddy :-) 03:34, 11 August 2006 (UTC)

Merchant Services/Bankcard Processing

Hi. I'm a new user of Wikipedia and find it cvery informative and this is about the next best thing since sliced bread. Now to the point. I'm and entrepreneur and an executive within the industry ont he acquiring side. Most of this article's dedicated tot he issuing side and that's fine however it doesn't entail it all. When a consumer visits a merchant to purchase a product or service with a credit card or a debit card, the merchant must have a terminal and the service to process that transaction. I understand the ins and the outs of this and could add plenty to this article. Also, I believe the ATM section can be further expanded including the ATM networks that are used to process ATM cards. Thanks. —The preceding unsigned comment was added by Diamonte (talk • contribs) 01:03, 2006 August 11.

- Go and add, your expertise is welcome! but please use sections and keep it organized. Also -- the ATM networks section probably belongs in other articles. There are articles on Automated teller machines and Interbank networks where those things probably belong.. —Cliffb 05:15, 11 August 2006 (UTC)

Shouldn't there be a list of credit card terms?

Shouldn't this article explain what the basic credit card related terms mean? I'm thinking something along the lines of one of these articles.

- www.ftc.gov/bcp/conline/pubs/credit/choose.htm FTC - Choosing and Using Credit Cards

- www.creditorweb.com/creditcards/articles/showarticle0091.html Understanding Credit Card Terms

- www.bankrate.com/brm/news/cc/20020906a.asp 15 must-know credit card terms

- Yes, I think it should. There's a credit card FAQ, which looks rather commercial, but may provide a good basis for this, so the link can be removed. Notinasnaid 17:42, 7 October 2006 (UTC)

- http://www.creditcards.com/credit-cards-glossary.php - Glossary of Common Credit Card Terms

(very thorough list)

Interwiki

I've noticed that the Interwiki links for this article, payment cards, debit cards, etc., are quite mixed up and in some cases, link to the wrong pages in the other language. This has to be rectified at some point in time. -Yupik 22:03, 14 September 2006 (UTC)

Customer Authentication

Some websites require knowing a phone number, full name, address, and credit card number.

As far as I can tell the only thing the merchant needs to carry out a transaction is a credit card number. Why are some websites demanding a phone number as a form of billing information? What is the minimum amount of information necessary to complete a transaction? ANONYMOUS COWARD0xC0DE 20:44, 24 September 2006 (UTC)

Typical authorisation process (magnetic stripe):

- PAN - card number (mandatory)

- Card expiration date (mandatory)

- CVV1 (track CVV) (mandatory)

- PIN (optional)

Voice authorisation:

- PAN (mandatory)

- ExpDate in embossed format (mandatory)

- CVV2 - embossed only on credit card (mandatory)

- a range of personal information (mandatory)

Internet payment authorisation:

- PAN (mandatory)

- ExpDate in embossed format (mandatory)

- CVV2 - embossed only on credit card (optional! It's a very rare mandatory!).

- a range of personal information (mandatory)

A "rang of personal information" depend on paranoia degree of an issuer bank. There are two types of operation:

- check account (booking hotel via Internet.. as example)

- payment operation (buy a goods via Internet).

I wrote about a payment operations. MikeKn 06:20, 30 March 2007 (UTC)

Ridiculous "fact" and citation ?

The claim that credit cards contributed significantly to the Great Depression and the citation given [5] seem so ridiculous that I believe it is either vandalism or naive silliness. Unless someone has a justification or counter-argument, I will remove this "fact" and citation within a few days. --Ben Best 08:18, 26 October 2006 (UTC)

- It struck me as odd. I have no way to check it, but looking at the citation "Academic class discussion" is not at all acceptable as a citation, as it is not verifiable. Notinasnaid 09:24, 26 October 2006 (UTC)

- User:Oxling [6] deleted the reference but not the "fact". I finished the job. --Ben Best 09:17, 27 October 2006 (UTC)

How they work - PIN authentication

The "How they work" section needs updating to explain about PIN authentication in merchant transactions. Also, the article seems to suggest that cards which have a chip onboard can function as both debit and credit cards. This is not always the case. DrHydeous 18:50, 26 October 2006 (UTC)

- I've added some details of PIN verification Adw2000 13:57, 17 January 2007 (UTC)

Merging Charga-plate with this article

We should merge Charga-plate with this article. --ŞρІϊţ ۞ ĨήƒϊήίтҰ (тąιк|соήтяївѕ) 04:31, 19 December 2006 (UTC)

- Thanks for your vote, If nobody puts up a good challenge, the articles will be merged after Jan. 1, 2007. -- Emana 18:43, 28 December 2006 (UTC)

Virtual credit cards

I could not see anything mentioned here on Virtual credit cards. There are lot of vendors of these cards online, some info on this will be use ful, may be a seperate topic also--59.93.11.38 09:06, 7 February 2007 (UTC)

Typicaly virtual credit card is set of information embosed on card without phisical "plastic" (PAN + ExpDate + CVV +...). Special case of "real" cards.

Transaction authorisations / security verification

How about some info on On-Line Authorisation? I understand that when your card is presented for payment, it is verified in real-time to your bank etc. that you a) aren't over your credit limit or b) the card isn't lost or stolen by way of a hotlist/stoplist.

This is a feature I'm fairly sure the CCs have pioneered and now debit cards use the same, as well as fuel cards I think. Any ideas? leopheard 13:20, 3 March 2007 (UTC)

"some info" added.. MikeKn 05:40, 30 March 2007 (UTC)

Convenience Charge

Should likely note that while most merchants are prohibited for charging credit card customers more for using a CC (to cover transaction charges) the Federal Government, and most states are required to. See irs and CreditCards.com. This is also the case for many colleges. The reason being that they are required to collect 100% of the charges. --Raccettura 01:40, 11 March 2007 (UTC)

Wall Street Journal Article

"How Graduates Can Maximize Their Finances" has some pointers for young adults on credit card use. Could be a good external link, although WSJ.com articles require a log-in. Any suggestions about how to add?

JMS1225 21:36, 7 May 2007 (UTC)

Trailing interest copyvio

Someone created a seperate article on trailing interest, but it was speedily deleted for copyright violation of http://www.the-creditcard-review.com/articles/credit_card_101/what_is_trailing_interest.htm . It was then pointed out that the same text comprises the corresponding section in this article. I didn't want to delete it without discussion, so I've tagged the section with a {{copypaste}} tag for now, but the section needs to be rewritten or deleted. Do other sections need to be loooked at? Thanks. --Finngall talk 20:28, 9 May 2007 (UTC)

I think it should be deleted. It's so poorly written. I doubt a few grammatical changes will fix the problem. I'll delete it in a few days if no one objects in the interim.--Roivas 15:37, 17 October 2007 (UTC)

Okay...section removed:

Trailing interest

A balance not paid in full by its due date will earn finance charges. If you then pay off the balance the next month it will also have an interest charge. If, for example, you charge $1000.00, receive the bill, and then decide to pay $500.00 by the due date, the next month's bill comes with a balance of $500.00 and the interest for the first month. If you pay the balance on the statement, the next month you will receive a bill with an interest charge for the balance on the account. A credit card balance accrues interest until the day it is paid. One way to avoid this problem if you are carrying a balance on your credit card and wish to pay it off, is to call your bank and ask for the payoff figure. You can generally speak to someone in customer service to get this number. Do not depend upon the voice system.

If someone wants to rewrite this, go for it. Remember, this is an encyclopedia. Maintain an acceptable level of legibility.--Roivas 15:20, 26 October 2007 (UTC)

Deferred Payment

Here's how credit cards work in my country, for both Visa and MasterCard credit cards. I don't know if there are many other countries that use this system, so I put it here for discussion:

You have a credit limit, for example 2500€. When you make a purchase of say, 500€, the merchant asks you how many months you wish to defer your payments into. If I say, for example, 5 months, the bank will charge me for 100€ each month, plus accumulated interests each month.

Combining all your purchases, and summing the minimum amount you have to pay for that month and their interests, you end up with what's called a "Minimum payment", that's the minimum amount of money you have to pay that month; and a "Total payment" which sums all the outstanding debt plus this month's interests. You then have to pay something between your minimum payment and your total payment. If you pay more than your minimum payment, the rest of the money is then usually distributed to the oldest debt you have.

Short-term payments are rewarded with lower interest rates, and there are some exceptions: For example, withdrawing from an ATM requires you to pay in full next month (the same thing as deferring for one month only); paying for gas works like this as well; making purchases abroad automatically defers the transaction to 12 months; purchases larger than a defined amount of money (like 5000€ or even more) can be deferred to 24, 36 or even 48 months with even greater interest rates.

This is in my opinion, a pretty good system, as you manage the duration of your debts. But careless management may lead to huge minimum payments or lots of money paid in interests for a long-term debt.

Now, if you fail to make a payment of at least your minimum payment, the outstanding amount enters for one month as special debt and you have to pay that, with interests, plus your minimum payment, as the next month's minimum payment. If you have a special debt for more than one month (actually becoming an unpaid debt for more than 60 days), the special debt keeps accumulating, but you are then reported to the credit bureaus, which erase your data -depending on your debt-, 2, 4, 5 or even 10 years after you pay your debt in full.

Oskilian 04:15, 20 June 2007 (UTC)

Standard Size?

Why does a credit card have the size it has? (8,4 x 5,4 cm). Jan Even. -- 143.97.2.35 (talk · contribs · logs) 09:40, 27 July 2007 (UTC)

- I am guessing it was similar in size to existing cards so that they would fit into wallets, and then the size was standardized to allow for machines to handle them like interact and ATM. Just a guess though. Sam Barsoom 20:04, 19 January 2008 (UTC)

Batching

The Batching part is incorrect. Whenever I run credit cards through an interac machine, the payments are completed immediately. We close the batches at the end of each day because it makes it easier to find missed transactions on the bank's side should the terminal and bank balances not equal when there are fewer transactions to check. It also gives us an idea of how much money we made from the cards each day. -- 63.139.73.5 (talk · contribs · logs)

Novation

Novation is a term that generally describes the replacement of one old debt (or contract) with a new debt (or contract), and requires the acceptance of both parties. Creditors often use Novation to change their terms by issuing you a written notice that states the new terms. The acceptance of the new terms (novation) occurs when the person continues to use the creditor's services after the specified date. In some laws/regulations/statutes, this is the only way to change those terms. Debtors can also use Novation to seek change to their terms by offering a written Novation letter to the creditor with specific changes, and those changes go into effect by positive action (such as the creditor not replying in a firm negative by a certain reasonable date or the deposit of the enclosed clearly labeled check or money order provided by the debtor to the creditor). -- 63.139.73.5 (talk · contribs · logs) 16:27, 10 August 2007 (UTC)

Medi Script

Would someone who knows something about credit card/service history please review Medi Script. Thanks. -- Jreferee (Talk) 19:37, 15 August 2007 (UTC)

Controversy section

Can someone define what it is that citibank pledged not to do? The sentence in question has a vague antecedent "this" after a sentence with a whole list of concerns. --69.202.71.21 16:12, 27 September 2007 (UTC)

Remove link Credit Card - The Official Site

The link to http://abc-of-credit-card.com should be removed. There is no information on the page. On the contrary it is flooded with ads. And how can a credit card have an official site? Happy 11:06, 8 November 2007 (UTC)

- You're correct. Way to be bold, by the way. Good job. --LeyteWolfer 17:55, 8 November 2007 (UTC)

co-branded cards

A better discussion of co-branded cards should perhaps be included.

The following quote may be useful:

Co-branding with Visa enables . . . you [to] learn more about your customers’ total spending behavior, by seeing all their purchases.

math error - bank interest in example is 200% not 10%

re: sect 5.1.1 interest expenses If a bank borrows 100 dollars at 5% it costs 5 dollars. If they then lend the 100 dollars at 15% they get 15 dollars. 15 dollars less the 5 dollar cost leaves them with 10 dollars profit. 10 dollars profit on 5 dollars is 200%. Anagus (talk) 03:58, 30 December 2007 (UTC)

- I think the profit is based on the principal borrowed and then lent as opposed to comparing the two interest rates. It says that this is the percent earned on the loan, called the "net interest spread". I think the key point is that the bank risks the entire amount borrowed in case of default, not just the interest they are being charged. The percent of profit is based on the whole investment, not just interest charges. I could be misunderstanding it though. Sam Barsoom 19:57, 19 January 2008 (UTC)

| This is an archive of past discussions about Credit card. Do not edit the contents of this page. If you wish to start a new discussion or revive an old one, please do so on the current talk page. |

| Archive 1 |

Credit Card Brands

What're all the different credit card brands or organizations that exist in the world? If there's a list or article anywhere I don't see it. This would be really useful information, as the only ones I can think of are American Express, Discover, Mastercard & VISA, and I'm sure a lot of that is due to my American perspective. Thanks caz | speak 20:53, 28 June 2007 (UTC)

- There's one called Diners Club and lots of national and regional brands. I can easily come up with at least 5 local credit card names in my country. Oskilian 21:43, 5 July 2007 (UTC)

- Diners Club cards, though, are issued by Mastercard. Where're you from that there are so many credit card companies? Like I said, a comprehensive list or article would really be useful on this subject. caz | speak 19:10, 7 July 2007 (UTC)

- To be honest, I think American Express, Mastercard and VISA are pretty much the biggest ones throughout the world. MasterCard and VISA are most prevalent here in the UK, with American Express also very common, though not quite as widely used (or indeed as widely accepted by merchants). I don't think the "Discover" brand exists here at all - if it does, it's very rare. —Preceding unsigned comment added by 217.155.138.250 (talk) 20:58, 12 February 2008 (UTC)

- Would be nice for someone to list the Schumer's_box (late fees and some of the more significant fine print) on cards from the major companies. Would this be legal? 69.3.28.216 (talk) 23:15, 29 December 2008 (UTC)

How Credit Cards Work complexity

This section seems to be pretty complex. As it's a complicated topic, this section could be further broken down to increase readability and understanding. Are there any finance geeks out there that could reorganize this section without losing validity and accuracy? Thanks. --Jophus00 (talk) 15:55, 28 March 2008 (UTC)

Formula Formatting

I think that some of the formulas need to be put into Tex...but I don't know how to use it... —Preceding unsigned comment added by 207.58.207.6 (talk) 16:34, 21 July 2008 (UTC)

Prepaid Cards

This section does not cover pre-paid department store credit cards. For example, all Macys associates are issued "Macy's Cards so they can get their employee discount, "if a young person gets a job at Macys, that person also gets a macys card. Most yooung people have either a weak credit history or none at all. For the associate discount to work, purchases must be made on the card. Associates with bad credit or no credit are given pre-paid cards. which have absolutely no fees and no "hooks" its basically a giftcard that you add money to, and use to get an employee discount. This card also has a $50-$75 "credit limit" that allows flexibility when making purchases. So can someone add in this information officially and with proper wording, because I'm not an English major. —Preceding unsigned comment added by 24.21.142.222 (talk) 07:44, 1 November 2008 (UTC)

issues

So the controversy section discusses issues related to people having too much debt. There is a flip side, namely when people don't get credit cards. Especially immigrants etc. A lot of transactions these days are mostly done using credit cards these days, so whoever does not have a credit card may not participate; not because of a lack of funding, but simply because one is disenfranchised by some unfair judgment/guidelines. —Preceding unsigned comment added by 67.204.33.62 (talk) 05:54, 22 December 2008 (UTC)

The credit card issuer is guarantying the good credit of the card holder. They cannot do that if a person does not have a credit history that shows an ability and willingness to make regular payments on time. One way of getting that credit history is to open a revolving account with a large store, buy something there on credit, make monthly payments on time, and then apply for a credit card. Some stores offer introductory credit cards to teens and other beginners if someone else with established credit cosigns for them. Greensburger (talk) 19:27, 22 December 2008 (UTC)

Two Proposals

1) I would like to propose a link to Debtors Anonymous-- A nonprofit organization that offers support groups for people with credit card addiction.

Credit card addiction is such a widespread problem that this link would be very relevant both to the article and to those who need help. Plus again they are nonprofit.

The web address (broken up, until approved, is www. debtors anonymous. org ).

2) I also would like to propose that the article have a section on credit card addiction. Millions of people have credit card addiction (not the majority, but a huge minority).

70.209.163.119 (talk) 21:28, 22 November 2009 (UTC)

- Pass on the link; that does not seem specific to the topic of the article. Thanks. If you can find reliable sources, please feel free to write a section on credit card addiction; with a preference to clinical sources as opposed to observational ones. Kuru talk 22:56, 22 November 2009 (UTC)

Thanks for the suggestion. There are tons of clinical references to credit card addiction. It is a real, clinically recognized syndrome.

71.215.92.226 (talk) 01:36, 11 December 2009 (UTC)

Minimum finance charge

Today I came to wikipedia to figure out what the term "Minimum finance charge" means. The page redirects to Credit card, which doesn't include this phrase anywhere. Maybe it should? ~ Booya Bazooka 04:27, 16 March 2009 (UTC)

- That page's history brought up this:

Nearly all credit cards have a minimum finance charge. You'll be charged that minimum if the calculated amount of your finance charge is less than that for any billing cycle. For example, your finance charge may be calculated (as a percentage of your balance) to be $0.35 but if the company's minimum finance charge is $1.00, you'll pay $1.00. A minimum finance charge applies only when you must pay a finance charge--typically*, when you carry over a balance from one billing cycle to the next. It is very important to understand that having a minimum finance charge does not mean that you will have to pay it every month even if you've paid off your balance in full or made no purchases. If you've paid off your balance in full or made no purchases you will not be charged anything. Typically, minimum finance charge is $0.50.

- Is the paid balance in full exclusion from finance charges a characteristic of ALL credit cards?

- I don't think it's important, so I won't be adding it to the article.--Elvey (talk) 18:56, 14 May 2009 (UTC)

- Just to note, this information is exactly why I came to this page also. Fortunately google now sends you here. Probably worth including. —Preceding unsigned comment added by 68.125.32.150 (talk) 18:51, 31 August 2009 (UTC)

History of credit cards & South Dakota (moved here from a deleted test page)

I believe it would be helpful if the article included something of the history of credit cards. At one point in time many States had usury laws which would have prohibited most of the interest rates charged today. My recollection is that sometime about the '60's, South Dakota sold its soul. The laws were changed and a large credit card company moved into the State. Since the Supreme Court has ruled that the laws of the State where the company is located apply, cardholders across the country became subject to South Dakota's new law.

I have been looking for additional information to verify my recollection, but have found precious little so far. If someone has more information I would love to hear it. —Preceding unsigned comment added by Richard13423 (talk • contribs)

- Your recollection is correct. Maybe PBS.org has reference material on a documentary they did on it.--Elvey (talk) 18:58, 14 May 2009 (UTC)

Credit card profits, debts, penalties

Here are some interesting facts (with additional references) from a April 23, 2009 Boston Globe article that could be verified and included in this article. Source is: www.boston.com/news/politics/politicalintelligence/2009/04/obama_calls_in.html

"Below is some background on the impact of credit cards on American families:

Prevalence of credit card debt

· Credit Card Debt has increased significantly in the past decade. Credit card debt has increased by 25 percent in the past 10 years, and reached $963B in January 2009. (Federal Reserve 2009)

· More than three-quarters of families have credit cards and close to half carry a balance. Seventy-eight percent of U.S. families have a credit card, and 44 percent of families carried a balance on their credit card. (Nielsen 2008, Federal Reserve 2008)

· Families carry significant credit card debt. The average amount of credit card debt among families with a balance was $7,300 in 2007 (the median was $3,000). (Federal Reserve, 2008)

· Delinquency rates have increased by more than a third since the end of 2006. The number of accounts more than 30 days late has increased from 3.9% in the fourth quarter of 2006, to 5.6% in the fourth quarter of 2008. (FFIEC, 2008)

Credit card fees and interest rates are extremely high

· Issuers collect $15B annually in penalty fees. Penalty fees on credit cards are around $15 billion annually, an estimated 10 percent of total credit card industry revenues. (Calculation based on GAO 2006 and Federal Reserve 2009)

· One-fifth of those carrying credit card debt pay an interest rate above 20 percent. Ninety-percent of issuers assessed variable rate cards and an estimated one-fifth were charged interest rates above 20 percent (GAO 2006)." 172.163.138.76 (talk) 09:20, 2 May 2009 (UTC)

Proposed External Link

I would like to propose adding the Frontline: secret history of the credit card link to the external links section of the article. Frontline —Preceding unsigned comment added by Pspadaro (talk • contribs) 20:17, 8 June 2009 (UTC)

- The link looks good in that it is apparently not promoting anything, but I couldn't really tell from the blurb what the one hour video would add to this article. I've only arrived here recently, but my guess is that there would be some resistance to adding links without good reason because it just invites another round of "me too" links. Is there a good reason? Johnuniq (talk) 23:43, 8 June 2009 (UTC)

I want to engage —Preceding unsigned comment added by 41.98.23.90 (talk) 10:53, 5 October 2009 (UTC)

Charga-plate

I note that Talk:Credit card/Archive 1#Merging Charga-plate with this article says

We should merge Charga-plate with this article. --ŞρІϊţ ۞ ĨήƒϊήίтҰ (тąιк|соήтяївѕ) 04:31, 19 December 2006 (UTC)

- Thanks for your vote, If nobody puts up a good challenge, the articles will be merged after Jan. 1, 2007. -- Emana 18:43, 28 December 2006 (UTC)

and the merge was effected on the 6th.

The language

- The Charga-Plate was an early predecessor to the credit card and used during the 1930s and late 1940s.

was added at some subsequent time.

While i have no reliable source in mind, it is a fact that charga-plates and credit-cards (without magnetic strips!) co-existed much longer, probably into the late 1950s. I'm changing the end date accordingly, and adding a fact tag.

--Jerzy•t 15:21, 18 March 2010 (UTC)

Related discussion at Electronic medical record

I've started a discussion at the electronic medical record page; please participate in the discussion there as the links being added here (see archived page) seem to be related and we can keep the discussion together. Thanks! Flowanda | Talk 20:49, 18 April 2010 (UTC)

Accruals

The following does not make sense: "However, most rewards points are accrued as a liability on a company's balance sheet and expensed at the time of reward redemption." In accounting, when this type of accrual is made on the balance sheet, it is expensed at the same time (debit expense credit accrual). You can't accrue something and expense it later. I think what the original editor meant to say was that when the banks accrue, they book a liablity, and this liability is relieved upon reward points redemption, at which point the bank would have to pay out cash. Anyway I took it out. —Preceding unsigned comment added by 207.238.152.3 (talk • contribs) 21:25, 16 January 2009 (UTC)

Missing interesting statistics

I came to this page anticipating some insight into how many credit cards there are (within the U.S. and worldwide), what percentage of the population own credit cards (since obviously some people own none and some people own many), and what portion of credit cards have carried over balances. That last fact is of particular interest to me, I would like to know if many people use credit cards simply as a convenience rather than as a means of achieving debt. I don't even see any suggestion of this sort of information in the See Also portion of this article.—Preceding unsigned comment added by MathInclined (talk • contribs) 03:57, 6 October 2009 (UTC)

Benefits to merchants

I would have thought one very obvious benefit for merchants is the extra turnover generated by the fact that the customer can purchase goods and/or services immediately and is less inhibited by the amount of cash in his or her pocket and the immediate state of his or her bank balance. A lot of the merchants' marketing is based on this immediacy. Maelli (talk) 10:44, 8 June 2010 (UTC)

Good suggestion. I copied your words into the article. Greensburger (talk) 21:06, 8 June 2010 (UTC)

External link suggestion

I'd like editors familiar with this page to consider this external link:

I removed it from Credit (finance), to which it's not relevant.

Pnm (talk) 23:48, 15 May 2010 (UTC)

Reverse conversion

3+3⁄8 in (85.73 mm) × 2+1⁄8 in (53.98 mm) Peter Horn User talk 02:32, 26 May 2010 (UTC)

"Transaction steps" citation

Consider citing to the following, both of which contain descriptions that are consistent with body text of this section: http://www.bankofamerica.com/small_business/merchant_card_processing/index.cfm?template=card_processing_basics http://www.creditcards.com/credit-card-news/how-a-credit-card-is-processed-1275.php <span style="font-size: smaller;" class="autosigned">—Preceding unsigned comment added by 66.166.188.234 (talk) 14:46, 29 July 2010 (UTC)</span><!-- Template:UnsignedIP --> <!--Autosigned by SineBot-->

Prepaid credit cards do not require a PIN?

Quote from this article: "Unlike debit cards, prepaid credit cards do not require a PIN." Is that always true? It may be true in the US and some other countries, but is this a real requirement for a prepaid credit card? I'm German and I ask because every German prepaid credit card from any German bank always requires a PIN. (These cards always lack embossing and there are always the words "for electronic use only" on these so called "Prepaid-Kreditkarten".) Are these cards no real prepaid credit cards? Is such a card a debit card? I'm really a bit confused now! ;) 188.192.101.163 (talk) 17:42, 11 August 2010 (UTC)

- These cards are real prepaid credit cards. All German prepaid credit cards are of the Mastercard or VISA brands, and debit cards from these two companies are marked with the word "Debit" somewhere on the card. The words "for electronic use only" only mean that the card isn't embossed. Therefore, either the magnetic stripe or the chip on the card has to be used to process a payment. Both is done electronically, of course. By the way, there are a few embossed prepaid credit cards without these four words on the German market. (However, I know only three such cards.) It is also not true that German cards always require a PIN. But German payment cards, like European payment cards in general, are virtually always "Chip and PIN"-cards. Today, virtually all transactions with Chip and PIN cards within Europe are processed via the EMV-chip on the card. Such Chip and PIN payments do, of course, always require a PIN, but it is still possible to use the card without the PIN where Chip and PIN payments are not available - In the U.S., for instance. 178.27.101.18 (talk) 02:59, 3 January 2011 (UTC)

History of Credit Cards

Thought it would be interesting to add a new section on the history of credit cards, analagous to what this author has put together http://www.thehistoryof.net/history-of-credit-cards.html <small><span class="autosigned">—Preceding unsigned comment added by Xs4-guy (talk • contribs) 13:57, 13 August 2010 (UTC)</span></small><!-- Template:Unsigned --> <!--Autosigned by SineBot-->

- Actually, it would be good to shorten and restructure the whole article, since it's so hard to navigate now. and one sub- or side-article should be History, another one Security problems and solutions. I'm german, so I won't do it ,-) Maximilian Schönherr (talk) 17:28, 6 March 2011 (UTC)

Dubious

CCs can be used instead of cash " for most purposes." - This vague (or universal) statement strikes me as dubious. While public transportation, some taxis, and most of the stores where I live will take (some) credit cards (not necessarily the one you have with you if you only have one), stands and people at the market do not. Very few vending machines here are set up to take CCs. Also, person-to-person transactions unrelated to commercial establishments are not yet done with CCs. So, I would say the articles statement should be researched or changed to some-thing like "for many purposes" or "in some places." Kdammers (talk) 00:29, 20 June 2011 (UTC)

Done. I deleted the dubious sentence because it duplicated the first sentence in the previous paragraph on convenience. Greensburger (talk) 00:35, 4 July 2011 (UTC)

Card-Not-Present

We now have several US suppliers demanding the "ATM PIN", ie the card PIN, for internet transactions. Presumably, this enables them to avoid the Card-Not-Present transaction fees. I haven't seen any documentation about this.

The Web is full of old documention saying that the PIN will not be required for Card-Not-Present transactions, and our (AUS) banks don't know anything about it either.

Any further information would be welcome.

Incidently, the section on Batching seems to imply that all credit cards processing is done by Batching. Clearly, this is no longer the case: many if not most merchants now use online processing. <span style="font-size: smaller;" class="autosigned">— Preceding unsigned comment added by 203.206.162.148 (talk) 03:19, 3 May 2012 (UTC)</span><!-- Template:Unsigned IP --> <!--Autosigned by SineBot-->

sample cc image

can someone add the key for the sample cc thats on the main page to the full size image page? @ http://en.wikipedia.org/wiki/File:Creditcardwcontactless.png<br /> 76.168.165.143 (talk) 02:09, 28 October 2012 (UTC)

{kind=link}

why is nothing about the size and shape of the card in here?

where did that originate from? — Preceding unsigned comment added by 198.240.212.2 (talk) 12:57, 31 January 2013 (UTC)

France

I'm wondering about the correctness of the description of the french situation regarding credit cards in this article, especially the line stating that you had to wait till the 90s to see any percentage like the US in terms of market penetration. I'm french and I have never seen a credit card in my life, only debit cards, so is there something I missed ? Is there any sign of credit cards being more accepted in our culture than in the 80s ? Consumer credits do seem to be a bit less a subject of social reject nowadays, but credit cards are extremely rare :s — Preceding unsigned comment added by 2A01:E34:EC03:EE40:97E:AD7F:853C:743B (talk) 12:03, 1 June 2013 (UTC)

Virtual credit cards?

I find no mentioning of virtual credit cards, such as the mywirecard MasterCard.

Feklee (talk) 08:39, 12 June 2013 (UTC)

Suggestion: Make more globally-balanced article.

As of today, the article seems to be very local to North America and UK. May I suggest to turn it into be globally balanced one?

未知との遭遇 (talk) 04:44, 30 August 2013 (UTC)

Controversy Section

Most of the information in the controversy section is unsourced. I suggest that we should move all that information to the talk page for now until we have some reliable sources to prove those claims.Jacob Pabst (talk) 15:45, 4 October 2013 (UTC)

Cutting cards

I remember in the 1980s there was the practice of merchants cutting cards in half with scissors if they were maxed out. This doesn't seem to happen any more, and indeed it always was a bit insane.

The article should make some mention of this, why and how it happened, and why and how it disappeared. Correctrix (talk) 05:52, 23 December 2013 (UTC)

Bellamy

- The concept of using a card for purchases was described in 1887 by Edward Bellamy in his utopian novel Looking Backward. Bellamy used the term credit card eleven times in this novel, although this referred to a card for spending a citizen's dividend from the government, rather than borrowing. Roughly similar in functions to the current day U.S. Social Security Cards with their Social Security numbers.

Bellamy's "credit card" is essentially a ration book. I've never used a Social Security card in any way remotely resembling either kind of credit card. —Tamfang (talk) 22:12, 25 May 2015 (UTC)

Comparison of credit card benefits in the US

In The Wiki Section 5.1.1 Comparison of credit card benefits in the US

This section is highly promotional material and is subjective according to the level of card the cardholder has. For example: a benefit in the grid may be offered on a reward card, but not on a traditional card, making it subject to being inaccurate with the frequent changes card issuers make to lure consumers to their respective cards. I would like to suggest that this section be removed and just state the basic:

Each card issuer makes available various benefits to lure consumers to their brand. As these benefits have numerous restrictions and limits. With this in mind we are not comparing promotional benefits within this article. More information on benefits offered by the different card brands may be found at:

AMERICAN EXPRESS: https://www.americanexpress.com/us/content/card-benefits/ DISCOVER: https://www.discover.com/credit-cards/resources/benefits

MASTERCARD USA: https://www.mastercard.us/en-us/consumers/features-benefits.html VISA USA: http://usa.visa.com/personal/card-benefits/index.jsp?b=1

wizbang_fl 00:43, 14 September 2015 (UTC)

External links modified

Hello fellow Wikipedians,

I have just added archive links to 3 external links on Credit card. Please take a moment to review my edit. If necessary, add {{cbignore}} after the link to keep me from modifying it. Alternatively, you can add {{nobots|deny=InternetArchiveBot}} to keep me off the page altogether. I made the following changes:

- Added archive https://web.archive.org/20080228043408/http://www2.tbo.com:80/content/2008/feb/15/bz-debit-cards-cash-in-on-rewards-riches/ to http://www2.tbo.com/content/2008/feb/15/bz-debit-cards-cash-in-on-rewards-riches/

- Added archive https://web.archive.org/20080322001627/http://www.minneapolisfed.org:80/pubs/region/06-06/interchange.cfm to http://www.minneapolisfed.org/pubs/region/06-06/interchange.cfm

- Added archive https://web.archive.org/20110711041436/http://www.lonelyplanet.com:80/tonywheeler/my_lists/why_we_cut_up_our_credit_cards/ to http://www.lonelyplanet.com/tonywheeler/my_lists/why_we_cut_up_our_credit_cards/

When you have finished reviewing my changes, please set the checked parameter below to true to let others know.

This message was posted before February 2018. After February 2018, "External links modified" talk page sections are no longer generated or monitored by InternetArchiveBot. No special action is required regarding these talk page notices, other than regular verification using the archive tool instructions below. Editors have permission to delete these "External links modified" talk page sections if they want to de-clutter talk pages, but see the RfC before doing mass systematic removals. This message is updated dynamically through the template {{source check}} (last update: 5 June 2024).

- If you have discovered URLs which were erroneously considered dead by the bot, you can report them with this tool.

- If you found an error with any archives or the URLs themselves, you can fix them with this tool.

Cheers.—cyberbot IITalk to my owner:Online 21:03, 23 January 2016 (UTC)

External links modified

Hello fellow Wikipedians,

I have just added archive links to 10 external links on Credit card. Please take a moment to review my edit. If necessary, add {{cbignore}} after the link to keep me from modifying it. Alternatively, you can add {{nobots|deny=InternetArchiveBot}} to keep me off the page altogether. I made the following changes:

- Added archive https://web.archive.org/20110723235456/http://blog.visa.com:80/2010/09/02/minimizing-confusion-over-minimums/ to http://blog.visa.com/2010/09/02/minimizing-confusion-over-minimums/

- Added archive https://web.archive.org/20110708074413/http://www.bmibaby.com/bmibaby/terms_and_conditions/our_top_booking_tips,_baby/fees_and_charges.aspx to http://www.bmibaby.com/bmibaby/terms_and_conditions/our_top_booking_tips,_baby/fees_and_charges.aspx

- Added archive https://web.archive.org/20090426033905/http://www.ecommerce-journal.com:80/news/14854_secure_pos_vendor_alliance_is_launched_by_hypercom_ingenico_and_verifone to http://www.ecommerce-journal.com/news/14854_secure_pos_vendor_alliance_is_launched_by_hypercom_ingenico_and_verifone

- Added archive https://web.archive.org/20060616211917/http://www.cardwatch.org.uk:80/media.asp?sectionid=4&pageid=109 to http://www.cardwatch.org.uk/media.asp?sectionid=4&pageid=109

- Added archive https://web.archive.org/20140106014436/http://www.federalreserve.gov:80/consumerinfo/wyntk_creditcardrules.htm to http://www.federalreserve.gov/consumerinfo/wyntk_creditcardrules.htm

- Added archive https://web.archive.org/20100327193555/http://www.oft.gov.uk:80/news/press/2006/68-06 to http://www.oft.gov.uk/news/press/2006/68-06

- Added archive https://web.archive.org/20131221014248/http://itools-ioutils.fcac-acfc.gc.ca/CCS-SCC/CCSearchCriteria.aspx?lang=eng to http://itools-ioutils.fcac-acfc.gc.ca/CCS-SCC/CCSearchCriteria.aspx?lang=eng

- Added archive https://web.archive.org/20081225210810/http://www.apacs.org.uk:80/resources_publications/card_facts_and_figures.html to http://www.apacs.org.uk/resources_publications/card_facts_and_figures.html

- Added archive https://web.archive.org/20110426125841/http://factfinder.census.gov:80/servlet/STTable?_bm=y&-geo_id=01000US&-qr_name=ACS_2007_3YR_G00_S0101&-ds_name=ACS_2007_3YR_G00_ to http://factfinder.census.gov/servlet/STTable?_bm=y&-geo_id=01000US&-qr_name=ACS_2007_3YR_G00_S0101&-ds_name=ACS_2007_3YR_G00_

- Added archive https://web.archive.org/20090115110602/http://www.foreignpolicy.com:80/story/cms.php?story_id=4207 to http://www.foreignpolicy.com/story/cms.php?story_id=4207

When you have finished reviewing my changes, please set the checked parameter below to true to let others know.

This message was posted before February 2018. After February 2018, "External links modified" talk page sections are no longer generated or monitored by InternetArchiveBot. No special action is required regarding these talk page notices, other than regular verification using the archive tool instructions below. Editors have permission to delete these "External links modified" talk page sections if they want to de-clutter talk pages, but see the RfC before doing mass systematic removals. This message is updated dynamically through the template {{source check}} (last update: 5 June 2024).

- If you have discovered URLs which were erroneously considered dead by the bot, you can report them with this tool.

- If you found an error with any archives or the URLs themselves, you can fix them with this tool.

Cheers.—cyberbot IITalk to my owner:Online 21:52, 23 February 2016 (UTC)

Visa, Inc. and Mastercard are banks? Or not? - Section 2.3 Usage: Parties Involved:

In this section the article states: "Credit card association: An association of card-issuing banks such as Discover, Visa, MasterCard, American Express, etc. that set transaction terms...". I thought I correctly understood that Visa and MasterCard are not banks, and do not issue credit, but rather serve as branded facilitators for such transactions. If that is correct, this should be changed. Sdg1969 (talk) 23:55, 28 February 2016 (UTC)Sdg1969

External links modified

Hello fellow Wikipedians,

I have just added archive links to one external link on Credit card. Please take a moment to review my edit. If necessary, add {{cbignore}} after the link to keep me from modifying it. Alternatively, you can add {{nobots|deny=InternetArchiveBot}} to keep me off the page altogether. I made the following changes:

- Added archive https://web.archive.org/20090426033905/http://www.ecommerce-journal.com:80/news/14854_secure_pos_vendor_alliance_is_launched_by_hypercom_ingenico_and_verifone to http://www.ecommerce-journal.com/news/14854_secure_pos_vendor_alliance_is_launched_by_hypercom_ingenico_and_verifone

When you have finished reviewing my changes, please set the checked parameter below to true or failed to let others know (documentation at {{Sourcecheck}}).

![]() An editor has determined that the edit contains an error somewhere. Please follow the instructions below and mark the

An editor has determined that the edit contains an error somewhere. Please follow the instructions below and mark the |checked= to true

- If you have discovered URLs which were erroneously considered dead by the bot, you can report them with this tool.

- If you found an error with any archives or the URLs themselves, you can fix them with this tool.

Cheers.—cyberbot IITalk to my owner:Online 21:48, 21 March 2016 (UTC)

Possible missing section

Should this article has a section about credit card terminals (or does such an article already exist)? Also, for historical reasons, it might be good to add a photo of "old school" non-electric manual imprinter (link to clarify what I mean by imprinter http://www.creditcardsupplies.net/Manual-Imprinters/Flatbed-2010-Date). • Sbmeirow • Talk • 20:55, 25 April 2016 (UTC)

- Yes there is already such an article at Payment terminal. Sargdub (talk) 19:58, 19 May 2016 (UTC)

Validation structure

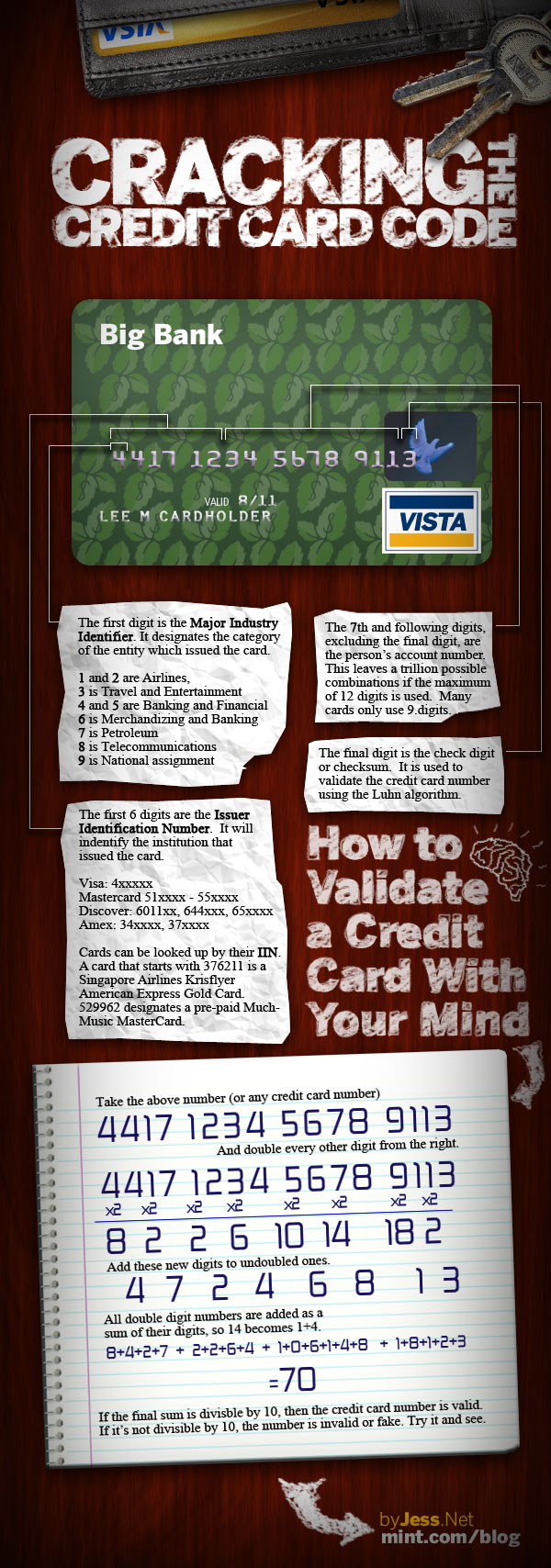

Can this be worked into the article?:

From: http://www.mint.com/blog/trends/credit-card-code-01202011/ → https://blog.mint.com/blog/wp-content/uploads/2011/01/CrackingCreditCode3.jpg (dead link, see below)

{kind=link}

1 2 3 4 - 5 6 7 8 - 9 0 1 2 - 3 4 5 6 <--- arrayA credit card number

1 3 5 7 9 1 3 5 <--- arrayB: odd number indexes: 1, 3, 5, ...

2 6 10 14 18 2 6 10 <--- array1: each index of arrayB doubled

2 6 1 0 1 4 1 8 2 6 1 0 <--- array1-1: array1: where ## ---> #,#

2 4 6 8 0 2 4 6 <--- array2: even number indexes: 2, 4, 6, ...

2 + 6 + 1 + 0 + 1 + 4 + 1 + 8 + 2 + 6 + 1 + 0 + 2 + 4 + 6 + 8 + 0 + 2 + 4 + 6 <--- string1: arithmetic to sum array1-1 + array2

If string1 is divisible by 10 then it is a valid number, else it is not.

JavaScript

http://www.adminsehow.com/wp-content/uploads/2011/03/CrackingCreditCode3.jpg

{kind=link}

http://htmledit.squarefree.com/

<code id="demo1">4417..1234--5678 9113</code><br>

<code id="demo2"></code><br>

<code id="demo3"></code><br>

<code id="demo4"></code><br>

<code id="demo5"></code><br>

<code id="demo6"></code><br>

<button onclick="myFunction()">Try it</button>

<script>

function myFunction() {

var str = document.getElementById("demo1").innerHTML;

var res = str.replace(/[\s-\.]+/g, "");

document.getElementById("demo1").innerHTML = res;

var res2nd = [res.charAt(0), res.charAt(2),

res.charAt(4), res.charAt(6),

res.charAt(8), res.charAt(10),

res.charAt(12), res.charAt(14),

res.charAt(16)];

document.getElementById("demo2").innerHTML = res2nd;

for (i = 0; i < res2nd.length; i++) {

res2nd[i] = Number(res2nd[i]) * 2;

}

document.getElementById("demo3").innerHTML = res2nd;

var res2ndSplit = [];

for (i = 0; i < res2nd.length; i++) {

if (res2nd[i].toString().length == "2") {

res2ndSplit.push(res2nd[i].toString().charAt(0));

res2ndSplit.push(res2nd[i].toString().charAt(1));

} else {

res2ndSplit.push(res2nd[i].toString());

}

}

document.getElementById("demo4").innerHTML = res2ndSplit;

var res2nd2 = [res.charAt(1), res.charAt(3),

res.charAt(5), res.charAt(7),

res.charAt(9), res.charAt(11),

res.charAt(13), res.charAt(15)];

document.getElementById("demo5").innerHTML = res2nd2;

var sum = eval(res2ndSplit.join(" + ") + " + " + res2nd2.join(" + "));

document.getElementById("demo6").innerHTML = sum;

if (eval(sum) % 10 == 0) {

alert("Valid, divisible by 10");

} else {

alert("Invalid, not divisible by 10");

}

}

</script>

—User 000 name 04:37, 25 May 2016 (UTC)

- I would say "no", for two reasons:

- 1. It would be fine to include that first diagram provided there were a verifiable and reliable source for it, but we cannot cite dead links or blogs in Wikipedia. So we can't use it with those sources.

- 2. Language specific source code also isn't appropriate in Wikipedia articles because we write for a general audience, not computer programmers. It might work as an example to demonstrate a feature of the language in an article about the language, but that isn't the case here. ~Amatulić (talk) 19:41, 26 May 2016 (UTC)

Merger proposal for Credit card register

The article Credit card register seems better off here at Credit card#Credit card register, considering the small amount of mergable content. - HyperGaruda (talk) 19:19, 12 March 2016 (UTC)

Usage of actual credit (not charge or debit) cards outside USA

Can we get some statistics on how many actual credit cards (cards with a rolling credit facility, so not charge cards or debit cards) are in use outside the USA? My impression is that, e.g., in Europe, use of such cards is limited to <1% of the population. The article itself even says most cards in Canada are charge cards. It seems hard to find any actual numbers, though. – gpvos (talk) 11:21, 18 February 2017 (UTC)

Photo request

| It is requested that a photograph be included in this article to improve its quality.

The external tool WordPress Openverse may be able to locate suitable images on Flickr and other web sites. |

Actual photos of credit cards would be illustrative, especially the early metal ones which look cool. -- Beland (talk) 21:14, 22 May 2018 (UTC) Beland (talk) 21:14, 22 May 2018 (UTC)

Edit revert

Why did my edits revert? Gulamsarwar269 (talk) 17:31, 17 February 2020 (UTC)

Is this link for people who already has an account? Because, I don't have 1. If that's so, what other link for me to add the topic? Please. — Preceding unsigned comment added by 95.175.85.38 (talk) 23:01, 26 September 2020 (UTC)

- No. If you are referring to people reverting you, it is because you are inserting information that either contradicts or isn't mentioned in the sources already cited in the article. If you have different sources, you need to cite them. If you keep getting reverted, explain your changes here. Don't just say what you are trying to change; we already know that. Explain your reasoning for the change, and state clearly what reliable sources are available that support the change you want to make. ~Anachronist (talk) 00:04, 27 September 2020 (UTC)