File:Subprime Crisis Diagram - X1.png

{kind=link}

{kind=link}

{kind=link}

Original file (960 × 720 pixels, file size: 17 KB, MIME type: image/png)

The examples and perspective in this article may not represent a worldwide view of the subject. (December 2010) |

{kind=link}

{kind=link}

Summary

[edit]{kind=link}

| Description |

Diagram of the Subprime Mortgage Crisis |

|---|---|

| Source |

I created this work entirely by myself. |

| Date |

October 10, 2008 |

| Author | |

| Permission (Reusing this file) |

See below.

|

Sources

[edit]{kind=link}

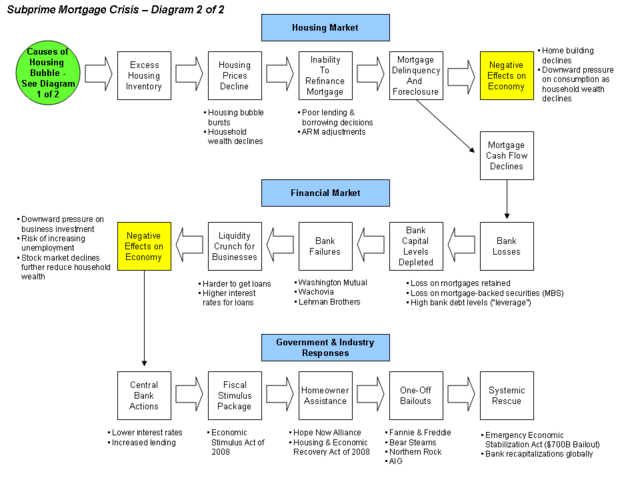

The many sources supporting this diagram are those used for the 2007 Subprime mortgage financial crisis and the linked articles below. Hopefully, this helps you visualize the elements. There is no substitute for reading the article first. This diagram is intended to illustrate how declines in the housing market transfer through the mortgage-backed securities to the financial markets, damaging the banks and economy along the way.

Text Explanation of the Diagram

[edit]{kind=link}

The ripple or domino effect was summarized in plain language by President Bush in his address to the Nation on September 24, 2008.[1]

- Housing Market: As the housing bubble burst in late 2006 and prices declined, mortgage holders counting on home price appreciation found themselves unable to pay their mortgages. Rates on adjustable-rate mortgages increased. Mortgage payment delinquency rates and foreclosures increased. With an oversupply of homes, housing construction declined. Housing value declines meant consumers had less money available for consumption. This placed downward pressure on economic growth, increasing the risk of recession.

- Financial Market: Mortgage-backed securities (MBS) derive their value from housing prices and mortgage cash flows. As these cash flows declined or became uncertain, financial institutions and investors holding MBS faced large losses. In certain cases, they had to sell these assets to pay off margin calls. Bank capital available for lending declined due to these losses. Several major banks and dozens of mortgage companies went out of business. Loans became more expensive (higher interest rates) or unavailable to those without stronger credit. Compared to the boom period, credit became considerably less available, placing downward pressure on both consumption and business investment.

- Government responses: Central banks have lowered interest rates to stimulate economies and make it more profitable for banks to loan. Tax rebates (stimulus package) were provided to U.S. taxpayers. Homeowners received assistance with re-financing their mortgages. Individual firms received bailouts and in September-October 2008 a comprehensive, global solution to "recapitalize" banks (e.g., to provide taxpayer funds in exchange for periodic dividend payments) was implemented. It is important to note that government actions took place throughout the 2007-2008 period, not just after the financial market impacts indicated. For example, the Federal Reserve lowered interest rates several times during various stages of the crisis.

Other Information

[edit]{kind=link}

- The aggregate demand side of the economic equation is: Consumption + Business Investment + Government Spending + Net Exports = Gross Domestic Product or GDP. The subprime crisis has erased $ trillions of household and stock market value, which places downward pressure on consumption (C), a key economic engine. In addition, liquidity or solvency concerns means bank loans are less available or more expensive for business investment (I), placing downward pressure on this engine. With the "C" and the "I" engines in the equation struggling, we are facing an enormous shock to the world economy, increasing the risk of global recession.

- As housing prices went up, people used homes like ATM's, borrowing against equity to use for consumer spending. When housing prices stopped appreciating and liquidity dried up, consumer spending and business investment slowed down, applying downward pressure to economic growth (GDP). This is the "real" or "main street" economy.

- High levels of debt or financial leverage across the household sector and financial system have made this crisis considerably worse, as the solvency of key financial institutions is a major factor. Certain financial institutions borrowed and lent enormous amounts of money relative to their cash or capital reserves, such as U.S. investment banks like Lehman Brothers.

- Alan Greenspan has said that until home prices have hit bottom, MBS values will be volatile and the crisis will continue.[2]

- Fortunately, there is a helpful series of historical precedents for financial sector bailouts to guide the international response. This is typically recapitalization, which involves the government providing cash to banks in exchange for preferred shares, which pay a dividend to the government. Economist Paul Krugman explained the crisis and bailout steps taken by banks around the world.[3][4] Time magazine summarized some of the lessons from previous Japan and Asia financial crises, which also included bank recapitalization as the primary solution.[5]

- See also Emergency Economic Stabilization Act of 2008 regarding the "$700 billion bailout" of September/October 2008.

Caveats

[edit]{kind=link}

- This diagram helps illustrate how a decline in housing prices ripples through the housing market and MBS to affect the banks. It does not show all the root causes of the problem.

- The diagram does not assign relative importance and key factors are not included. Some factors are critical to the housing market or the financial markets; some are critical to both. Experts disagree on which factors matter most.

- The many elements of the diagram interact and provide feedback on each other to varying degrees. This is a very simplistic representation. It would take a rather complex computer simulation to show the interaction of the two meta markets--the housing market and the financial market.

Sources

[edit]{kind=link}

The letters from Fed Chairman Bernanke provide a helpful explanation of the subject.[6] [7]

Further, several cover stories and in-depth articles appeared in the Economist[8] [9] [10] and Business Week.[11]

Former Federal Reserve Chairman Greenspan wrote an Op Ed piece for the Wall Street Journal that summarizes the crisis from a variety of angles.[12]

Economist Joseph Stiglitz summarized his views on the causes of the crisis.[13]

Image of the Housing Bubble

[edit]{kind=link}

This diagram can be better understood in the context of the housing bubble. The subprime mortgage crisis followed the bursting of the United states housing bubble.

References

[edit]{kind=link}

- ^ NYT Transcript-President Bush Speech of September 24, 2008

- ^ The Wall Street Journal Online - Featured Article

- ^ Krugman - NYT

- ^ Krugman - NYT - Gordon does Good

- ^ Time Magazine - Lessons from Japan & Asia

- ^ FRB: Speech-Bernanke, Financial Markets, the Economic Outlook, and Monetary Policy -January 10, 2008

- ^ FRB: Speech-Bernanke, The Recent Financial Turmoil and its Economic and Policy Consequences-October 15, 2007

- ^ The credit crunch | Postcards from the ledge | Economist.com

- ^ CSI: credit crunch | Economist.com

- ^ America's economy | Getting worried downtown | Economist.com

- ^ Housing Meltdown

- ^ The Wall Street Journal Online - Featured Article

- ^ Stiglitz-Vanity Fair

Licensing:

[edit]{kind=link}

| This work is licensed under the Creative Commons Attribution-ShareAlike 3.0 License. |

| Permission is granted to copy, distribute and/or modify this document under the terms of the GNU Free Documentation License, Version 1.2 or any later version published by the Free Software Foundation; with no Invariant Sections, no Front-Cover Texts, and no Back-Cover Texts. |

| The uploader or another editor requests that a local copy of this file be kept. This image or media file may be available on the Wikimedia Commons as File:Subprime Crisis Diagram - X1.png, where categories and captions may be viewed. While the license of this file may be compliant with the Wikimedia Commons, an editor has requested that the local copy be kept too. This file does not meet CSD F8 and should not be tagged as a Commons duplicate. If you desire to nominate it for deletion, notify the tagging editor. |

{kind=link}

File history

Click on a date/time to view the file as it appeared at that time.

| Date/Time | Thumbnail | Dimensions | User | Comment | |

|---|---|---|---|---|---|

| current | 02:40, 21 October 2008 | | 960 × 720 (17 KB) | Farcaster (talk | contribs) | |

| 06:59, 10 October 2008 |  | 960 × 720 (16 KB) | Farcaster (talk | contribs) | ||

| 05:44, 10 October 2008 |  | 960 × 720 (16 KB) | Farcaster (talk | contribs) | ||

| 05:30, 10 October 2008 |  | 960 × 720 (16 KB) | Farcaster (talk | contribs) | ||

| 05:18, 10 October 2008 |  | 960 × 720 (16 KB) | Farcaster (talk | contribs) | {{Information |Description=Diagram of the Subprime Mortgage Crisis |Source=I created this work entirely by myself. |Date=October 10, 2008 |Author=~~~~ |other_versions= }} |

You cannot overwrite this file.

File usage

The following file is a duplicate of this file (more details):

{kind=link}

- File:Subprime Crisis Diagram - X1.png from Commons

The following 4 pages use this file:

{kind=link}