File:Long-term interest rates (eurozone).png

Size of this preview: 492 × 599 pixels. Other resolutions: 197 × 240 pixels | 394 × 480 pixels | 836 × 1,018 pixels.

Original file (836 × 1,018 pixels, file size: 228 KB, MIME type: image/png)

| This is a file from the Wikimedia Commons. Information from its description page there is shown below. Commons is a freely licensed media file repository. You can help. |

Summary

| Description |

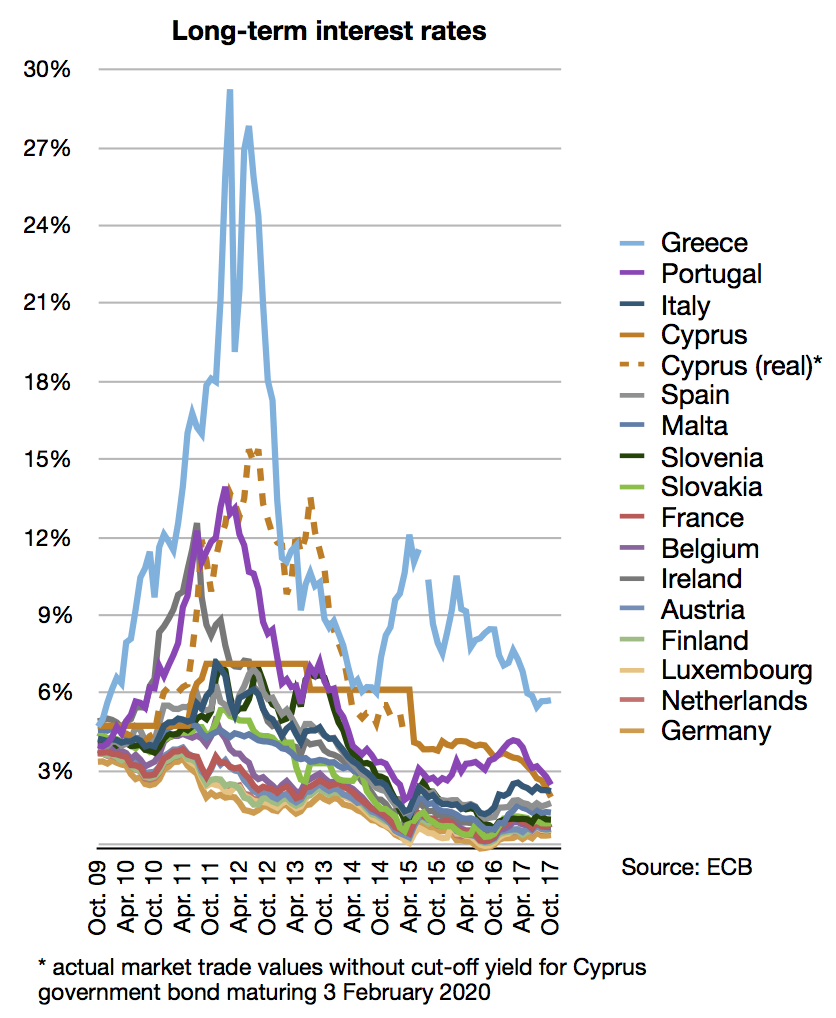

English: Long-term interest rate statistics (monthly averages of secondary market yields - percentages per annum - of government bonds with maturities close to ten years) for all Eurozone countries, except the three Baltic states. Latvia and Lithuania were not included because of only joining the eurozone after the debt crisis had erupted, while the exclusion of Estonia is due to its absence of issued government long-term debt (ECB notes: "As Estonia has a very limited government debt, there are currently no suitable long-term government bonds available on the financial market"). In regards of Cyprus, ECB chose only to publish primary market yield data for its long term government debt (with the effective yield being fixed to the one applying on the issuing date of the government bond with the longest 10 year maturity), but as the accuracy of these data can be questioned (i.e. private creditors holding maturing Cypriot bonds, were forced to exchange them with the latest issued 2023 bond at a fixed 6.0% rate), the graph also feature a dotted line for Cyprus of its secondary market (freely stock exchange traded) long-term yield extracted from its bond with maturity on 3 February 2020 (see note below). Source: http://www.ecb.int/stats/money/long/html/index.en.html

|

| Date | |

| Source | Own work |

| Author | Spitzl |

| Other versions |

|

.png)

-ar.png)

{kind=link}

{kind=link}

{kind=link}

.png){kind=link}

|

This chart image could be re-created using vector graphics as an SVG file. This has several advantages; see Commons:Media for cleanup for more information. If an SVG form of this image is available, please upload it and afterwards replace this template with

{{vector version available|new image name}}.

It is recommended to name the SVG file “Long-term interest rates (eurozone).svg”—then the template Vector version available (or Vva) does not need the new image name parameter. |

Licensing

I, the copyright holder of this work, hereby publish it under the following licenses:

|

Permission is granted to copy, distribute and/or modify this document under the terms of the GNU Free Documentation License, Version 1.2 or any later version published by the Free Software Foundation; with no Invariant Sections, no Front-Cover Texts, and no Back-Cover Texts. A copy of the license is included in the section entitled GNU Free Documentation License. |

This file is licensed under the Creative Commons Attribution-Share Alike 3.0 Unported, 2.5 Generic, 2.0 Generic and 1.0 Generic license.

- You are free:

- to share – to copy, distribute and transmit the work

- to remix – to adapt the work

- Under the following conditions:

- attribution – You must give appropriate credit, provide a link to the license, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use.

- share alike – If you remix, transform, or build upon the material, you must distribute your contributions under the same or compatible license as the original.

You may select the license of your choice.

File history

Click on a date/time to view the file as it appeared at that time.

.png&dir=prev){kind=link}

.png&offset=20160702160955){kind=link}

.png&offset=&limit=20){kind=link}

.png&offset=&limit=50){kind=link}

.png&offset=&limit=100){kind=link}

.png&offset=&limit=250){kind=link}

.png&offset=&limit=500){kind=link}

| Date/Time | Thumbnail | Dimensions | User | Comment | |

|---|---|---|---|---|---|

| current | 07:59, 26 November 2017 | | 836 × 1,018 (228 KB) | Spitzl | fix Cyprus |

| 21:19, 25 November 2017 |  | 836 × 1,023 (230 KB) | Spitzl | fix color code | |

| 21:09, 25 November 2017 |  | 849 × 1,033 (232 KB) | Spitzl | fix white space | |

| 21:06, 25 November 2017 |  | 1,753 × 1,240 (265 KB) | Spitzl | update | |

| 08:46, 19 July 2017 |  | 865 × 1,052 (232 KB) | Spitzl | update | |

| 10:26, 18 March 2017 |  | 838 × 1,028 (239 KB) | Spitzl | update | |

| 22:05, 9 January 2017 |  | 821 × 1,016 (236 KB) | Spitzl | update | |

| 22:00, 2 October 2016 |  | 1,156 × 1,423 (185 KB) | Cmdrjameson | Compressed with pngout. Reduced by 157kB (46% decrease). | |

| 16:21, 2 July 2016 |  | 1,156 × 1,423 (342 KB) | Spitzl | fix graph | |

| 16:09, 2 July 2016 |  | 369 × 620 (73 KB) | Spitzl | update |

File usage

The following 3 pages use this file:

Global file usage

The following other wikis use this file:

- Usage on ar.wikipedia.org

- Usage on ast.wikipedia.org

- Usage on da.wikipedia.org

- Usage on el.wikipedia.org

- Usage on es.wikipedia.org

- Usage on eu.wikipedia.org

- Usage on fa.wikipedia.org

- Usage on fr.wikipedia.org

- Usage on fr.wikinews.org

- Usage on gl.wikipedia.org

- Usage on id.wikipedia.org

- Usage on ko.wikipedia.org

- Usage on no.wikipedia.org

- Usage on pa.wikipedia.org

- Usage on ps.wikipedia.org

- Usage on pt.wikipedia.org

- Usage on ro.wikipedia.org

- Usage on sq.wikipedia.org

- Usage on th.wikipedia.org

- Usage on tr.wikipedia.org

- Usage on zh-yue.wikipedia.org

- Usage on zh.wikipedia.org

.png){kind=link}